Article Series

UK manufacturers failing CBAM verified data checks and CSRD double materiality audits are almost always using spend-based estimation for Scope 3 Category 5 — a methodology that no third-party verifier will accept.

The fix requires three things: a gravimetric waste audit producing stream-level tonnage data, EWC-coded disposal route confirmation for each stream, and DEFRA 2025 emission factors applied by disposal route. Total infrastructure cost for most mid-size sites: £12,000–£16,000. CBAM default-value penalty exposure avoided: ongoing and compounding.

Applies to: UK manufacturers with EU export exposure (CBAM-covered sectors), companies in CSRD scope or supplying CSRD-in-scope EU customers, and any facility building a verified SBTi Category 5 baseline. Does not apply to: Scope 1 on-site combustion calculations, Category 12 end-of-life treatment of sold products, or inert construction waste (EWC Chapter 17).

Why Is Your Scope 3 Category 5 Inventory Failing CBAM Auditors — and What Does a Compliant Waste Carbon Baseline Actually Require?

UK manufacturers with EU export exposure face a Category 5 measurement problem that is quietly becoming a financial liability. If your Scope 3 inventory was built using spend-based estimation, it will not survive a CBAM verified data challenge — and under CSRD's double materiality framework, that same methodology may have led your team to mark waste emissions as immaterial when the activity-based numbers tell a very different story. For the full picture of where Category 5 sits within your broader UK manufacturing waste compliance costs and regulatory obligations, start with our compliance guide first — it covers the cost landscape, the regulatory timeline, and every major obligation that intersects with your waste streams.

This article is part of the Zero-Emission Industrial Waste Treatment series — covering non-combustion waste treatment across industrial, manufacturing, and regulatory contexts.

This article covers the narrower, more urgent territory: how to measure Category 5 correctly, what infrastructure a gravimetric audit actually requires, and what CBAM verification and CSRD assurance teams are looking for when they arrive.

What Is Scope 3 Category 5 — and Why Does Every Major Compliance Framework Now Require Activity-Based Measurement?

GHG Protocol Category 5 covers all waste generated at your facilities during operations — landfill disposal, incineration (energy-from-waste), recycling, composting, and on-site treatment. It does not cover waste from use of your sold products (Category 12) or waste from your supply chain (Category 1). It covers only the waste your own sites generate.

The GHG Protocol defines three calculation methods for Category 5 in strict preference order:

- Method 1 — Supplier-specific: Your waste contractor provides allocated Scope 1 and 2 emissions directly. Highest accuracy; requires active contractor engagement.

- Method 2 — Waste-type-specific: You multiply the mass of each waste type by disposal-route-specific emission factors (kg CO₂e/tonne). Requires knowing composition and destination by stream.

- Method 3 — Average-data: Total waste mass multiplied by average factors by disposal route, without type differentiation. Acceptable, but carries higher uncertainty.

Spend-based estimation — multiplying your waste management spend by an economic input-output factor — is not listed as a primary method for Category 5. The GHG Protocol's 2024 Scope 3 Proposals explicitly recommended phasing it out across all categories.

This applies when you are reporting Scope 3 under GHG Protocol, submitting CBAM data to EU importers, setting SBTi targets, or completing a CSRD double materiality assessment. It does NOT apply if you are calculating Scope 1 emissions from on-site combustion (a separate calculation entirely) or reporting downstream emissions from the use of your sold products.

Scenario: A precision engineering firm generating 340 tonnes of waste annually across mixed metals, oily rags, contaminated packaging, and canteen food waste. Using Method 3 with average factors produces a Category 5 figure of approximately 14 tCO₂e. Switching to Method 2 with DEFRA disposal-route factors — knowing 60 tonnes go to landfill, 180 tonnes to EfW, 100 tonnes recycled — produces a figure of 31 tCO₂e, more than double. That difference is material to a double materiality assessment screening. It is also the difference between a credible SBTi Category 5 disclosure and one that a validator will flag.

Why Does CBAM Explicitly Reject Spend-Based Estimation — and What Does Verified Data Actually Mean?

CBAM requires installation-level, process-specific embedded emissions data. Spend-based proxies are not a permitted methodology under the Implementing Regulation.

The EU Carbon Border Adjustment Mechanism entered its definitive phase on 1 January 2026. UK manufacturers exporting steel, aluminium, cement, fertilisers, or hydrogen to EU customers must now provide emissions data that meets these four requirements:

- Installation-level specificity: Data must come from the specific plant producing the exported goods — not a company average, sector average, or national benchmark.

- Process-level breakdown: Embedded emissions must be separated by production process (e.g., direct reduction vs. blast furnace for steel).

- Activity-based calculation: Either a calculation-based approach using actual fuel consumption, material inputs, and laboratory analyses — or a measurement-based approach using continuous emission monitoring. Financial proxies are not compliant at any stage.

- Third-party verification: Reports require verification by an accredited body applying a 5% materiality threshold.

The regulation enforces an 80/20 rule: at least 80% of reported embedded emissions must use actual installation data. No more than 20% may rely on default values. When default values are used, the Commission's proposed escalating surcharge schedule — currently under delegated act review — would apply a penalty markup to those defaults. Exact rates will be confirmed in final delegated legislation; the structural principle is clear and locked: defaults are penalised, and the penalty is designed to escalate over time to drive adoption of verified reporting.

The first annual CBAM declaration covering 2026 imports is due 30 September 2027. A proposed expansion to approximately 180 downstream steel and aluminium products takes effect from 1 January 2028.

This applies to any UK manufacturer exporting CBAM-covered products or embedded CBAM-covered materials to EU importers. It does NOT apply to non-CBAM sectors (food, textiles, chemicals, pharmaceuticals), to exports destined for non-EU countries, or to manufacturers with no EU customer relationships.

Scenario: A mid-size UK steel fabricator. Their EU importer requests CBAM data for the first declaration in September 2027. The fabricator's sustainability team has reported Scope 3 Category 5 using spend-based estimation for three years. This methodology produces no installation-level activity data, no process-specific breakdown, and no audit trail a third-party verifier can sign off. The importer is forced to submit default values. The proposed surcharge markup applies to the difference between the inflated default and actual embedded emissions — a direct cost borne by the importer, who will pass it back through the commercial relationship.

How Does Spend-Based Estimation Create a Category 5 Materiality Blind Spot in CSRD Double Materiality Assessments?

When companies use spend-based emission factors to screen Category 5, they systematically understate waste emissions — and then exclude the category from further analysis on the basis of that understatement.

Here is the sequence of the flaw:

- Sustainability team runs ESRS double materiality screening across all 15 Scope 3 categories using spend-based EEIO factors.

- Waste management spend at manufacturing sites is typically low relative to other cost categories — £50,000 to £200,000 annually for a mid-size plant. EEIO factors applied to this spend produce an apparently small Category 5 figure.

- The category is scored below the materiality threshold and marked "not significant."

- No further measurement is conducted. No activity-based calculation is commissioned.

- The result is a self-fulfilling exclusion: because spend-based estimation understated the emissions, the category was never measured accurately enough to reveal its actual scale.

When companies switch to Method 2 using actual tonnages and DEFRA disposal-route factors, Category 5 emissions commonly come in 2–10× higher than spend-based estimates — particularly where significant volumes go to landfill, where EfW handles organic fractions with high biogenic content, or where hazardous waste streams have not been segregated.

Under CSRD's ESRS framework — specifically ESRS E1 for climate and ESRS E5 for resource use and circular economy — this methodology risk is now an audit exposure. Assurance providers conducting limited assurance reviews can challenge the screening methodology directly. If spend-based estimation led to the exclusion of a category that activity-based data would have flagged as significant, the double materiality assessment itself is vulnerable to challenge. The 2026 Omnibus package revised CSRD scope thresholds (non-EU parent companies should verify their specific threshold position against the recently revised thresholds in the final transposed text), but value chain data pressure remains: in-scope EU companies will continue requesting Category 5 data from UK suppliers regardless of whether the UK supplier has independent CSRD obligations.

This applies when CSRD applies directly to your company, or when you are a material supplier to an EU company in scope. It does NOT apply if you are entirely outside EU supply chains and have no voluntary ESG reporting obligations.

Scenario: A UK composite materials manufacturer supplies to a Tier 1 German automotive OEM. The OEM is CSRD-in-scope and requests Category 5 data for its own value chain inventory. The UK manufacturer's sustainability manager finds Category 5 marked "not material" in their last double materiality assessment, justified by a spend-based screening note. The OEM's ESG audit team flags this as a methodology gap. The UK manufacturer now faces an emergency retrospective waste audit with a four-week deadline to the OEM's reporting cycle.

In My Experience: The Double Materiality Assessment That Nearly Missed a CBAM Exposure

I was reviewing a mid-size UK specialty chemicals manufacturer's CSRD double materiality assessment — 340 employees, three sites, significant EU export revenue. The sustainability team had done genuinely careful work across most of the ESRS topics. But Category 5 had a single note in the screening spreadsheet: "assessed as not material based on waste spend relative to total Scope 3." The spend figure was £118,000 across all sites. The spend-based EEIO calculation gave them a Category 5 figure of around 11 tCO₂e. Against their Scope 1+2 of 4,200 tCO₂e, it barely registered.

I asked them to pull the Waste Transfer Notes for the previous twelve months. Three sites. Twelve months. What came back was 680 tonnes of waste, of which 290 tonnes was organic process waste and contaminated solvents going to a merchant incinerator at £380 per tonne gate fee. Another 180 tonnes of mixed non-hazardous was going to a regional landfill at £152 per tonne all-in. The remaining 210 tonnes was recycled or recovered.

When I ran the Method 2 calculation using the appropriate DEFRA factors, the Category 5 figure was 38 tCO₂e — not 11. Still not large in absolute terms. But the issue was not the emissions number. The issue was this: the same incinerator contract was the disposal route for a fraction of their embedded waste in goods exported to a German customer — and that German customer's procurement team had just sent a CBAM data request. The incinerator was providing a quarterly tonnage receipt. It was not providing installation-level emissions data by process. There was no activity-based audit trail. There was no way to separate the embedded emissions from the waste treatment component of the exported product costs.

The company was six months from their first reportable CBAM period. The fix was not expensive — it was a waste audit, a contractor data request, and a methodology upgrade. But it had to happen before the declaration deadline, not after.

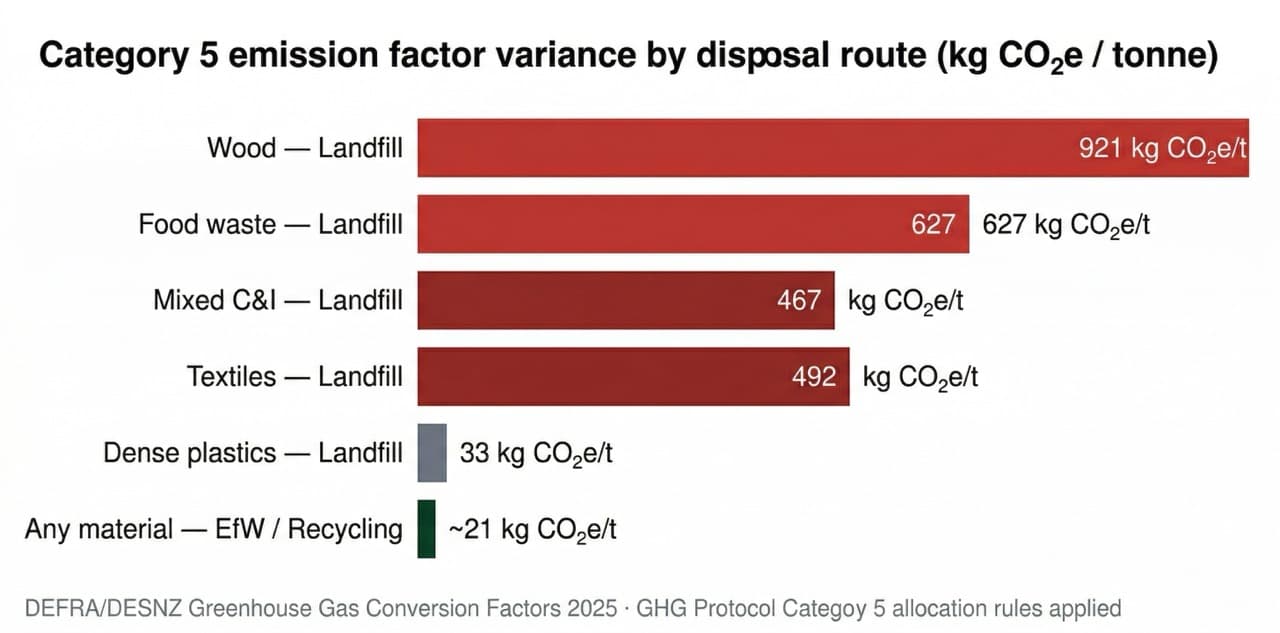

What Emission Factors Does DEFRA Publish for Different Waste Disposal Routes — and How Much Does the Choice of Disposal Route Change the Category 5 Calculation?

The choice of disposal route has a larger effect on Category 5 than almost any other variable. DEFRA's annual Greenhouse Gas Conversion Factors (published by DESNZ) reveal variance of up to 44× between the worst and best disposal options for the same waste type.

Key emission factors from the DEFRA 2025 dataset (kg CO₂e per tonne):

| Waste type | Landfill | EfW / Combustion | Recycling |

|---|---|---|---|

| Mixed C&I waste | ~467 | ~21 | ~21 |

| Food waste | ~627 | ~21 | — |

| Wood | ~921 | ~21 | ~21 |

| Dense plastics (HDPE) | ~33 | ~21 | ~21 |

| Textiles | ~492 | ~21 | ~21 |

The EfW and recycling figures appear low (~21 kg CO₂e/tonne) because DEFRA follows GHG Protocol allocation rules: stack emissions from energy-from-waste are attributed to the energy consumer, not the waste producer. For Category 5 purposes, the waste generator's exposure is primarily the landfill-route factor where applicable.

For the full greenhouse gas balance analysis by disposal route — including avoided burden credits for recycled materials and the embedded carbon implications of each treatment pathway — see our carbon footprint impact guide.

This applies to all organic, mixed C&I, and wood-based waste streams. It does NOT apply to inert waste (construction rubble, excavated soil) classified under EWC Chapter 17, which carries a different lower-rate landfill tax treatment and negligible biogenic methane emission.

Scenario: A food-ingredient manufacturer sending 80 tonnes of organic process waste to landfill annually. Using the mixed C&I average factor (~467 kg CO₂e/tonne): 37.4 tCO₂e Category 5 contribution from that stream alone. Switch the same volume to an EfW contractor: 1.7 tCO₂e. The disposal route choice produces a 22× difference in the reported emissions figure — and a corresponding difference in the CSRD disclosure, the SBTi baseline, and the CBAM audit trail.

What Infrastructure Does a Gravimetric Waste Audit Require — and What Does One Actually Cost to Implement?

A gravimetric waste audit is the systematic process of physically separating, weighing, and categorising waste streams by mass. It produces the site-specific, stream-level tonnage data every compliant Category 5 calculation requires.

The core infrastructure:

- Calibrated weighing equipment — Platform or floor scales (300–600 kg capacity) at approximately £300–£1,500 per unit; wheelie bin weighing systems at £1,000–£2,500; weighbridges for high-volume sites at £15,000–£80,000 installed.

- EWC-coded segregation at source — Labelled bins or skips by EWC code at point of generation. Pre-segregation is the single biggest determinant of data accuracy; bulk mixed waste post-sorting produces far less reliable composition data.

- Digital recording — Itemised waste management platforms provide barcode-scanned bin identification, weight capture at each collection, and automated monthly reports by stream and disposal route.

- Waste Transfer Note reconciliation — Quarterly reconciliation of WTN tonnages against scale weights, with EWC codes confirmed against contractor manifests. This produces the activity-based audit trail CBAM verification requires.

The professional external waste audit — where a consultant physically sorts and weighs a representative sample over one to two weeks — typically costs £2,000–£10,000 depending on site complexity and number of waste streams. Annual calibration of weighing instruments runs £100–£500 per unit under BS EN 45501. The total ongoing cost for a well-instrumented site is typically £3,000–£8,000 per year including staff time, calibration, and software licensing.

This applies to any manufacturer needing to move from average-data or spend-based estimation to Method 2 waste-type-specific calculation. It does NOT apply if your waste contractor already provides Method 1 supplier-specific emissions data — verify this against your current contract before commissioning an audit.

Scenario: A plastics processor with four waste streams (mixed plastics, contaminated film, cardboard, and process sludge) across two sites. A two-week waste audit costs £6,500. Installation of bin-mounted weighing terminals: £4,200. Digital recording platform licence: £1,800/year. Total Year 1 cost: £12,500. This produces a Category 5 baseline certified to ±10% accuracy — sufficient for CBAM verified data requirements, CSRD assurance, and SBTi progress tracking.

What Is the Step-by-Step Process for Building a Category 5 Baseline That Will Survive Third-Party Verification?

A verifiable Category 5 baseline requires five documented steps. Attempting to calculate it without completing all five produces a figure that a third-party auditor will not sign off.

Step 1 — Waste audit: Complete a gravimetric audit covering a minimum 12-month period (or representative sampling extrapolated to annual totals). Document methodology, sample representativeness, and any estimation assumptions.

Step 2 — EWC classification by stream: Map every waste stream to a six-digit EWC code. Cross-reference codes against Waste Transfer Notes. Identify any streams currently lumped under generic codes (e.g., 20 03 01 — mixed municipal waste) that should be disaggregated.

Step 3 — Disposal route confirmation: For each stream, confirm the disposal route from contractor documentation — landfill site permit number, EfW plant permit number, or recycling facility permit number. A verbal assurance from a contractor is not sufficient for third-party verification.

Step 4 — Emission factor application: Apply DEFRA's current-year factors to each stream × tonnage × disposal route. Document the factor version used. Retain the DESNZ source publication reference.

Step 5 — Assurance trail assembly: Compile Waste Transfer Notes, contractor disposal confirmations, weighing records, factor references, and calculation methodology into a single verification pack. For CBAM purposes, this must be available to the EU importer's CBAM declarant on request.

This applies to manufacturers building a Category 5 inventory for CBAM, CSRD, SBTi, or voluntary ESG reporting. It does NOT apply to Scope 1 on-site combustion calculations or to Category 12 end-of-life treatment of sold products — those are separate inventory items.

Scenario: A UK textile manufacturer. Step 1 reveals 210 tonnes of cut-waste fabric going to landfill annually (EWC 04 02 09). Step 2 confirms correct EWC coding. Step 3 confirms disposal to a specific permitted landfill. Step 4: 210t × 492 kg CO₂e/tonne (DEFRA 2025 textiles to landfill factor) = 103.3 tCO₂e — a material Category 5 number by any threshold. Step 5 produces a verification pack the company's CSRD auditor signs off in two hours.

How Should UK Manufacturers Prioritise Category 5 Compliance Work Given CBAM, CSRD, and SBTi Deadlines Running Simultaneously?

Priority should follow financial exposure, not reporting elegance. The deadlines are not evenly spaced.

The recommended sequencing:

- Immediately: Run a spend-to-activity-based sanity check. Pull Waste Transfer Notes for the last 12 months, total tonnages by disposal route, and re-run Category 5 using Method 3 average factors. If this figure is more than 2× your current spend-based number, the category is mis-stated in existing disclosures.

- Q2–Q3 2026: Commission a professional waste audit across all manufacturing sites. This establishes the baseline that feeds all three frameworks simultaneously.

- Q4 2026: Install stream-level weighing infrastructure and digital recording. This converts the one-off audit into a continuous monitoring capability.

- January 2027: First full Category 5 inventory using Method 2 covers the 2026 reporting year — in time for CSRD disclosures, SBTi progress reports, and the September 2027 CBAM declaration.

- Ongoing: Review DEFRA emission factors annually (published each June). Update disposal route confirmations at every contract renewal.

This timeline applies to manufacturers with EU export exposure and/or CSRD reporting obligations taking effect for the 2026 financial year. It does NOT apply to companies with no EU supply chain relationships and no voluntary reporting frameworks — though mandatory digital waste tracking (April 2027) will require gravimetric data regardless.

Scenario: A mid-size UK engineering manufacturer, 2,400 tonnes of waste annually, EU exports representing 38% of turnover. Running the sanity check in April 2026 reveals Category 5 is understated by 3.4×. Waste audit commissioned May 2026 (£8,500 cost). Weighing infrastructure installed August 2026 (£7,200). First verified Category 5 inventory ready November 2026. CBAM data pack assembled December 2026, ready to supply EU importers before the September 2027 declaration deadline. Total compliance infrastructure cost: £15,700. CBAM default-value penalty exposure on 38% of turnover: avoided entirely.

The Problem Behind the Problem

You now understand the immediate issue clearly: your Category 5 inventory was built on a methodology that no third-party auditor — CBAM verifier, CSRD assurance provider, or SBTi validator — will accept without challenge. Switching to activity-based measurement will fix the reporting gap. But there is a deeper structural problem that gravimetric audits alone will not resolve.

UK manufacturers are failing Category 5 audits not because they lack sustainability intent — but because waste carbon has never been measured at stream level, and the waste streams generating the most exposure are the ones least visible in a spend-based system. Organic process waste, contaminated mixed fractions, and high-moisture industrial residues are cheap to dispose of in absolute terms but carry extremely high landfill methane factors. They look small in a spend screen. They are large in an emissions calculation. And because they are typically handled by a single bulk waste contractor on a single mixed-stream contract, there is no granular data in the contractor's documentation to work with — only a quarterly tonnage receipt.

The root cause is not the measurement tool. It is the disposal model. When waste leaves your site on a single mixed-stream contract to a landfill or merchant incinerator, you have surrendered control of the data at the point of collection. No amount of gravimetric auditing on your side can produce a verified emission profile for what happens after the waste leaves your gate — because the emission event happens at the disposal facility, under someone else's operational control.

That is the problem PHANTOM's subcritical water hydrolysis process is designed to eliminate. Request a technical consultation → By converting the waste stream from an off-site disposal liability into an on-site treatment cycle, the entire emission event happens within your facility boundary — under your operational control, documented by your monitoring systems, and verifiable by your auditors. The process operates at 180°C under controlled pressure, breaking down organic matter in a sealed vessel with no stack emissions, no dioxins, and no methane generation. The output is a sterile, low-volume residue with a fully documented treatment cycle. For Category 5 reporting purposes, this means the activity data — temperature, pressure, cycle duration, input mass — is generated on-site and retained in your own records. CBAM verification does not require contractor documentation. CSRD assurance does not require disposal facility permit tracing. SBTi progress tracking does not require annual supplier engagement requests. You own the audit trail.

The Bottom Line on Category 5 Compliance for UK Manufacturers

Scope 3 Category 5 compliance is not an abstract reporting exercise. UK manufacturers exporting to the EU face a real CBAM financial exposure that compounds annually as the CBAM factor escalates toward 100% of embedded emissions by 2034. CSRD assurance risk is real for any manufacturer in a European supply chain whose Category 5 was screened using spend-based estimation. And the gravimetric infrastructure required to fix both problems is not a multi-year programme — it is a measurable cost, deliverable within a single planning cycle.

The practical next step for most manufacturers is a retrospective waste audit covering the 2025–2026 period, followed by the installation of stream-level weighing infrastructure before the April 2027 mandatory digital waste tracking deadline. These two steps together produce the activity-based inventory that satisfies every framework in parallel.

If your operation generates more than 500 tonnes of organic or mixed waste annually, the economics of the PHANTOM industrial waste treatment machine make the audit trail question irrelevant — because on-site subcritical water hydrolysis treatment converts the disposal liability into a documented, internally controlled process with zero contractor dependency and a verified emission profile your auditors can review without leaving your facility.

Scope 3 Category 5 Reporting Readiness Checklist

⚙️ Manufacturing Waste Carbon Readiness Checklist

Assess your facility's waste carbon readiness across four critical domains.

📊 Measurement

- Waste audit completed (last 12 months)

- All streams classified by material type and mass (kg/tonne)

- DEFRA or EPA WARM emission factors applied per stream

- Scope 3 Category 5 baseline calculated and documented

- Waste carbon data integrated into ESG report

⚖️ Regulatory

- EU CBAM monitoring infrastructure in place (if exporting to EU)

- UK Plastic Packaging Tax registration confirmed (if applicable)

- EU PPWR (Aug 2026) packaging recyclability assessed

- UAE/Saudi Arabia GCC emissions reporting timeline mapped

- US state-level regulations mapped (CA, WA, NY, MA) — independent of federal

🔄 Process & Operations

- 5R hierarchy review completed for top 3 waste streams

- Waste segregation system operational at point of generation

- Recycling contracts in place with certified, tracked operators

- Diversion rate % tracked and reported monthly

- Operations team trained on segregation protocols

🚀 Advanced & Technology

- IoT / gravimetric capture on all major waste streams

- Carbon management software integrated with waste data

- On-site treatment technology evaluated for organic / mixed waste

- Zero Waste to Landfill (UL 2799 / TRUE) certification pathway assessed

- Industrial symbiosis partnerships explored with adjacent facilities

Ready to eliminate landfill and incineration from your waste strategy? Phantom Ecotech's subcritical water hydrolysis technology converts organic, plastic, medical, and mixed industrial waste into recoverable outputs — zero dioxins, zero flue gas, verified Scope 3 reduction.

Request a Technical Consultation →Frequently Asked Questions

GHG Protocol Category 5 covers all waste generated at your own facilities during operations — landfill disposal, incineration (energy-from-waste), recycling, composting, and on-site treatment. It does not cover waste from use of sold products (Category 12) or supply chain waste (Category 1). The preferred calculation method is Method 2: waste mass by type multiplied by DEFRA disposal-route-specific emission factors.

CBAM requires installation-level, process-specific embedded emissions data. Spend-based proxies are not a permitted methodology under the Implementing Regulation. At least 80% of reported embedded emissions must use actual installation data; no more than 20% may rely on default values, which carry a proposed escalating penalty surcharge under delegated act review.

A professional external waste audit covering a representative sample over one to two weeks typically costs £2,000–£10,000 depending on site complexity. Annual calibration of weighing instruments runs £100–£500 per unit. Total ongoing cost for a well-instrumented site is typically £3,000–£8,000 per year including staff time, calibration, and digital recording platform licensing.

The DEFRA 2025 dataset assigns approximately 467 kg CO₂e per tonne for mixed commercial and industrial waste to landfill — versus approximately 21 kg CO₂e per tonne for the same material sent to EfW or recycling. This 22× variance between disposal routes makes disposal route data mandatory for accurate Category 5 calculation.

The first annual CBAM declaration covering 2026 imports is due 30 September 2027. A proposed expansion to approximately 180 downstream steel and aluminium products takes effect from 1 January 2028. UK manufacturers should have activity-based Category 5 data ready before December 2026 to allow their EU importer to meet the deadline.

Sources: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard; DEFRA/DESNZ Greenhouse Gas Conversion Factors 2025; EU CBAM Implementing Regulation (EU) 2023/1773; ESRS E1 Climate Change and ESRS E5 Resource Use and Circular Economy; SBTi Corporate Manual v2.0; Environment Agency Digital Waste Tracking implementation timeline.

Figures are for informational purposes only and do not constitute legal, financial, or regulatory advice. CBAM delegated act rates are subject to finalisation. CSRD scope thresholds reflect the 2026 Omnibus revision — verify your company's specific position against the final transposed text. ~1.27 USD/GBP.